Nasdaq's Shame

How to rig an index to appease a billionaire

Disclaimer: The following article is for informational purposes only and represents the opinion of the author. It should not be construed as investment or any other kind of advice. All information is based on publicly available data believed to be accurate as of the date of publication, but the author makes no representations or warranties as to its completeness or accuracy. Readers should conduct their own research and due diligence and don’t rely on anonymous goofballs on the internet for anything. Thank you for your attention to this matter.

"When buying and selling are controlled by legislation, the first things to be bought and sold are legislators." - P.J. O’Rourke

I’m generally a fan of index investing for most people. Historically, indexing was a brilliant, low-cost way for investors to free-ride on the price discovery done by active managers (longs and the occasional evil ladder-attacking short seller). The market did the hard work of figuring out what a company was worth, and the index fund simply bought a representative slice of the market. The index was the tail; price discovery was the dog.

Today, the tail is violently wagging the dog. And the dog has the shits. Trillions of dollars are blindly sloshing around in passive funds, and index inclusion dictates market structure rather than reflecting it.

Enter the whores (metaphorically speaking) at Nasdaq.

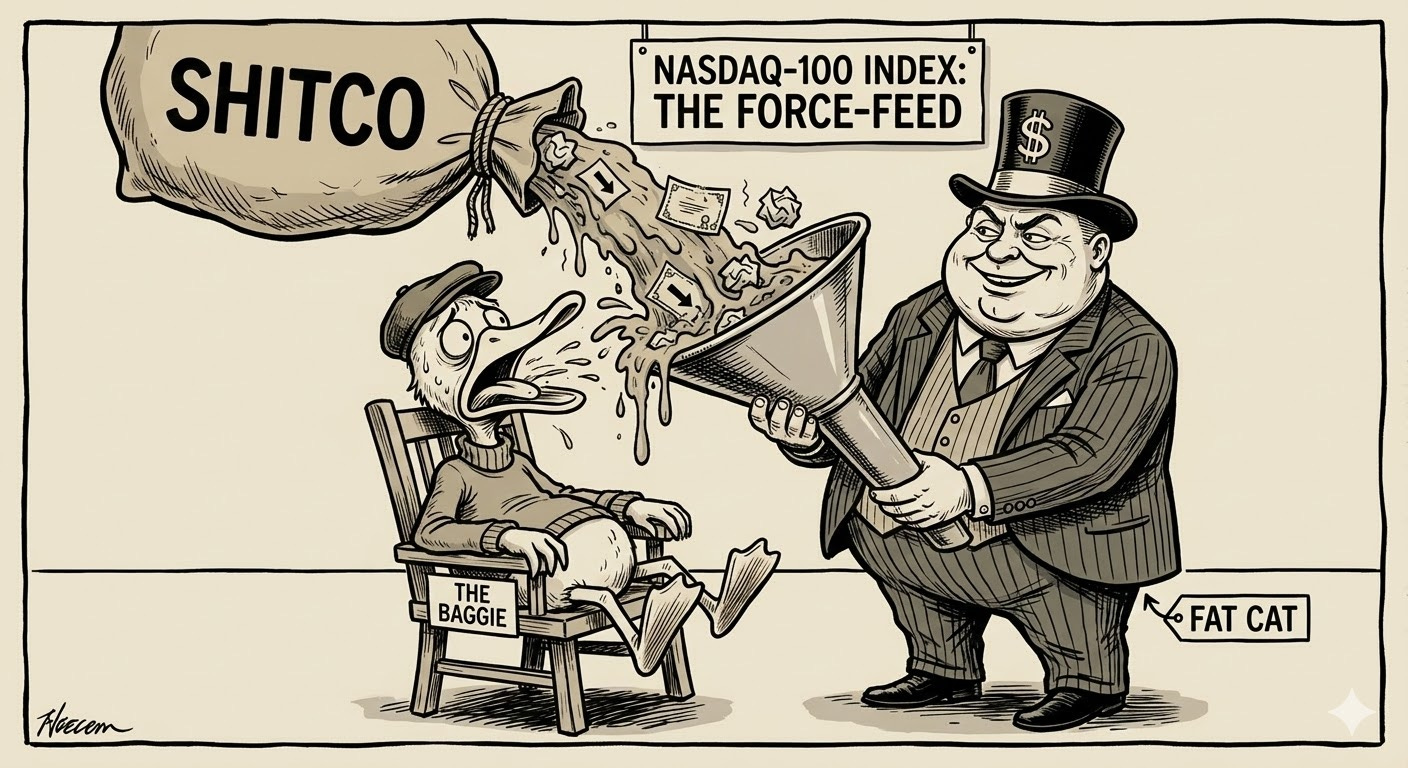

Nasdaq recently circulated a Nasdaq-100 Index “Consultation” (located here). They are officially seeking feedback from investors on proposed updates to their index methodology. But let’s be real: this “consultation” is Nasdaq-speak for letting us know what they are going to force feed us, like a baggy foie gras duck. A thinly-veiled blueprint for how to forcefully transfer wealth from the retirement accounts of passive retail investors directly into the pockets of corporate insiders and early investors.

Source: Google (not a shitco) Gemini Nano Banana 2

Why the sudden urge to rewrite the rulebook? Because Elon Musk’s SpaceX is gearing up for an IPO with a reported target valuation of around $1.75 trillion. To win this lucrative listing over the NYSE, they appear to be shamelessly bending the knee to a specific demand by SpaceX (per Reuters) for near-immediate index inclusion. This rule change will also give Nasdaq a leg up over the NYSE on subsequent large IPOs (think OpenAI, or Anthropic as examples).

Let’s look at the actual proposed rules in this consultation document, because it is an absolute masterclass in structural market manipulation.

The “Fast Entry” Exemption

Currently, large companies newly listed via IPO aren’t added to the index in a timely manner. Nasdaq wants to “fix” this supposed problem that just mysteriously cropped up the moment SpaceX announced its IPO plans, with a “Fast Entry” rule. Under this rule, any newly listed company whose entire market capitalization ranks within the top 40 current constituents gets announced with at least five days’ notice and added to the index after just fifteen trading days.

Crucially, the company will be entirely exempt from the standard seasoning and liquidity requirements.

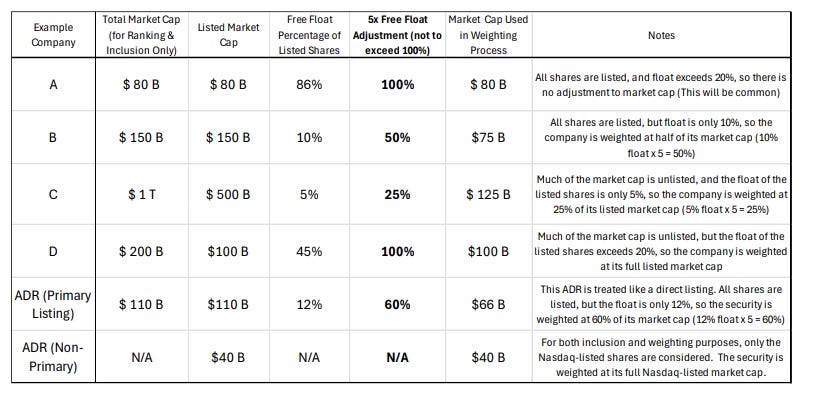

The 5x Multiplier for Low-Float Stocks

Here is the smoking gavage gun. In the exact same document, Nasdaq proposes a new approach for including and weighting “low-float” securities, defined as those below 20% free float.

For context, a saner index like the S&P 500 is strictly “free-float adjusted,” meaning it only weights a company based on the shares actually available for the public to trade. Nasdaq, on the other hand, uses a methodology that factors in all shares, including locked-up insider shares that aren’t even for sale—and their proposed “fix” for this low-float problem is where the math gets truly diabolical.

Under this new proposal, each low-float security’s weight will be mechanically adjusted to five times its free float percentage, capped at 100%.

Source: Nasdaq

Let’s see how this actually works.

Assume SpaceX IPOs at a $1.75 trillion valuation. To keep things simple, assume the company floats 5% of the shares to the public ($87.5 billion worth of tradable stock). The other 95% is subject to a standard lock-up period and cannot be traded.

Under Nasdaq’s proposed 5x multiplier rule, the company’s index weight would be calculated at 25% of its total market cap (5% float x 5), even though only 5% is available for trading. If they float only 5% of the shares, the weighting would be 25% (about $438 Billion). 15% would be $1.3 Trillion.

So, on Day 15, passive Nasdaq-100 ETFs (like the QQQ) and mutual funds are mathematically forced to buy allocations of this stock as if it were, in the 5% example, a $438 billion company.

And here is the real kicker: those figures assume the stock stays flat from the IPO price. It won’t. Active traders and hedge funds will aggressively front-run this guaranteed, price-insensitive bid. If the stock rallies 40% in those first two weeks, passive funds aren’t buying based on the IPO price—they are buying based on the Day 15 market price. They will be forced to blindly allocate capital at whatever insane price it trades up to.

The index is applying a phantom, mega-dollar weighting to a restricted, tightly-held float. Tens of billions of dollars of price-insensitive, passive capital are legally mandated to aggressively bid for the stock over a matter of days. You are effectively forcing a firehose of mega-cap index capital through a garden hose of actual liquidity. It is a recipe for a massive, artificial supply-and-demand squeeze.

The Lock-Up Illusion

Some may argue “But the lock-up period is 180 days! The initial index squeeze happens on Day 15. The market will have months to find real price discovery before the insiders can actually sell!”

Nonsense.

Yes, the initial Day 15 squeeze will inevitably cool off. But by waiving the seasoning period and jamming this low-float behemoth into the index immediately, you have completely corrupted the baseline. You’ve forced passive indexers to buy at the absolute top of an engineered liquidity squeeze. You have established a manipulated, artificially elevated price floor fueled by forced buying.

For the next five months, the stock will be based on a highly distorted market structure, driven in part by continued passive inflows (barring a market meltdown). And here is where the math gets truly sadistic.

Nasdaq’s proposed rules explicitly state that float figures are only updated during scheduled quarterly rebalances. And what happens when a company’s float goes above 20%? The 5x multiplier is dropped, and the company is upgraded to a full, 100% index weighting.

So, if you are His Nibs, how do you play this? You time your lock-up expiration right before a quarterly index rebalance.

The moment the lock-up expires, the physical float jumps from 5% to 15% (in our examples) to 100%. At the very next rebalance, Nasdaq updates the math, and the passive funds are mechanically forced to increase their allocation from that artificial 25-75% (again, in our examples) weighting up to the full 100%.

They are legally mandated to aggressively buy billions of dollars more of the stock the exact moment the insiders are able to flood the market with their unlocked shares. Can you feel your baggy liver turning to foie gras yet?

I’m not alleging any particular wrongdoing by SpaceX and Nasdaq here. Why wouldn’t SpaceX use its (legal) leverage to push Nasdaq around? And Nasdaq is perfectly entitled to feed what’s left of its credibility into the Cathiewoodchipper.

I don’t think the company is focused on (legally) extorting Nasdaq for early index inclusion because of the initial 15 days. I believe they are focused on the lockup expiry and ensuring that it coincides with a massive forced bid. The smaller the initial IPO float, the more powerful the rebalance will be.

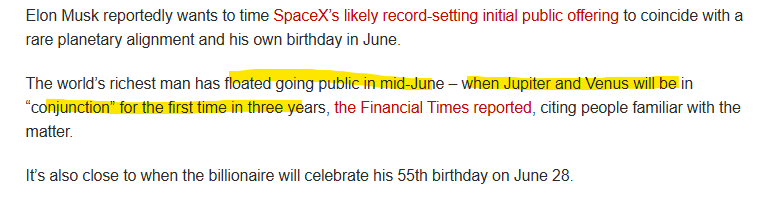

To hit the December 18, 2026 quarterly rebalance date for the Nasdaq 100, SpaceX needs to IPO around mid-June. You will no doubt be shocked to learn that, indeed, SpaceX is targeting, ahem, mid-June for its IPO.

Source: New York Post, referencing The Financial Times

To seemingly throw prospective baggies off the scent, “people familiar with the matter” have apparently leaked the purported reason for a mid-June IPO: The alignment of Jupiter and Venus.

Source: New York Post

Can’t make this shit up. Jupiter and Venus. F*ck me.

I would not at all be surprised to see the company issue additional shares into the forced index buying, potentially competing with its own investors to soak up that demand.

Nasdaq has promised to publish a “summary” of comments that it received during the comment period. Perhaps Nasdaq will, in its final determination, conclude that the integrity of its indexes is paramount, and not implement this change. Perhaps the SEC will step in and attempt to block it, to protect investors, right?

Source: Goodfellas

“If you’re playing a poker game and you look around the table and can’t tell who the sucker is, it’s you.” - Paul Newman

I wrote this article myself, and it expresses my own personal opinions only. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. It is not a recommendation to buy, sell, short, hold, or avoid any security. It should not be relied upon for any purpose other than entertainment. Numbers and analysis presented have not been proof-read or independently verified. Assume I am a goofball. I’ve been called worse by better than you. Despite my best efforts I make mistakes. I do get it wrong sometimes.

A new Keubiko substack article is a damn good way to start a Tuesday.

Been saying it for awhile: NASDAQ is just OTC+